What is Equipment Breakdown Insurance?

Justin Sonon • August 14, 2025

Should you add this affordable coverage to your home insurance?

What Equipment Breakdown Coverage Can Provide If Added to Your Home Insurance Plan

Most homeowners understand that their standard home insurance protects against things like fire, theft, and certain weather damage. But what happens when your furnace stops working in the middle of winter or your refrigerator suddenly dies? Standard homeowners insurance often won’t cover mechanical or electrical failures, and that’s where Equipment Breakdown Coverage comes in.

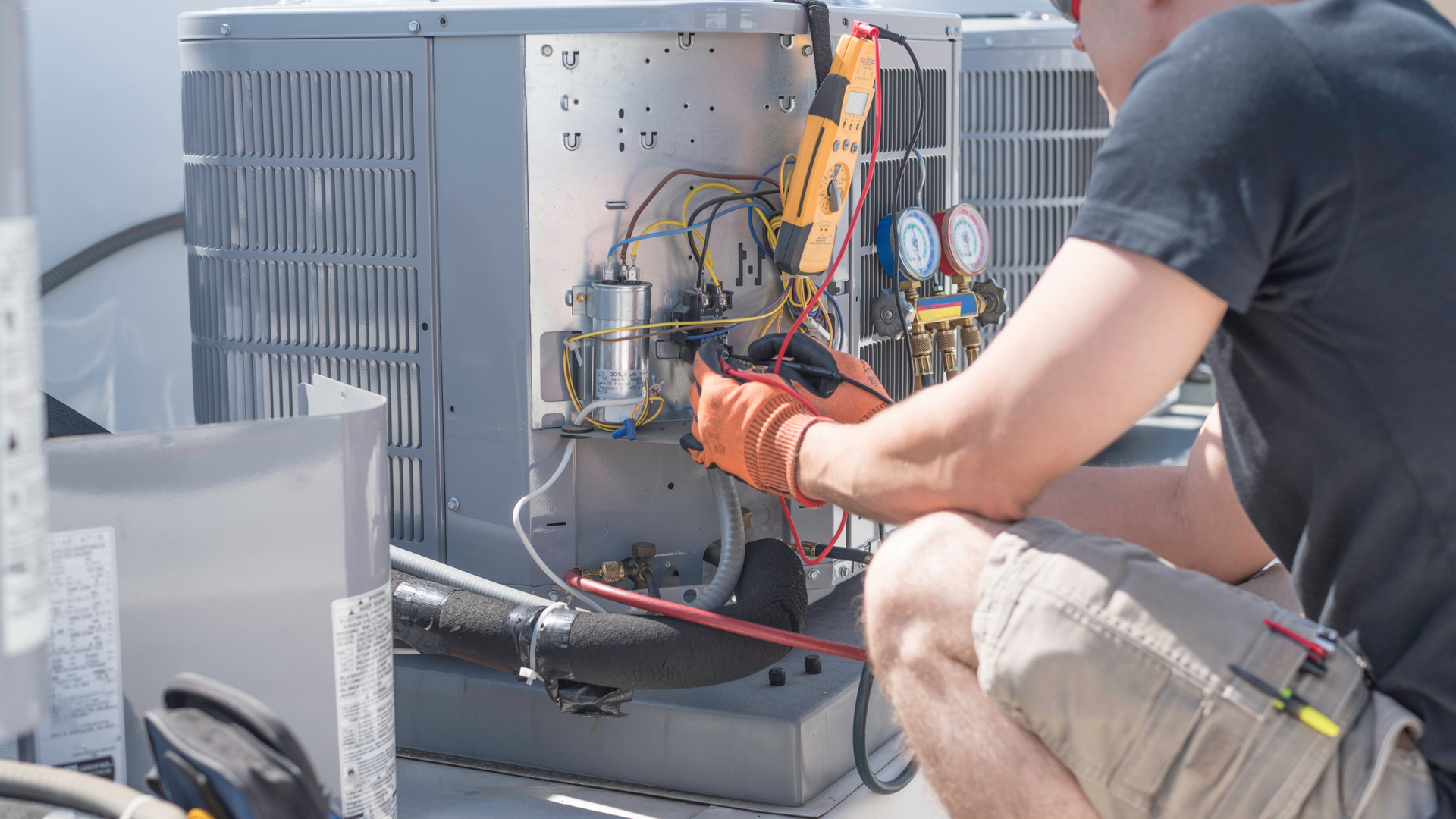

What Is Equipment Breakdown Coverage?

Equipment Breakdown Coverage

is an optional add-on to your home insurance policy that helps pay for the repair or replacement of essential household systems and appliances if they break down due to a sudden, unexpected mechanical, electrical, or pressure-system failure.

It’s not a maintenance plan, as it won’t cover normal wear and tear, but it does step in for unexpected failures that could otherwise cost thousands out of pocket.

What Does It Cover?

While coverage details can vary by insurer, here are common items protected under Equipment Breakdown Coverage:

Heating and Cooling Systems: Furnaces, boilers, central air conditioning units, and heat pumps.

Kitchen Appliances: Refrigerators, freezers, ovens, dishwashers, and more.

Laundry Appliances: Washers and dryers.

Electrical Systems: Panels, wiring, generators, and certain smart home devices.

Water Heaters and Well Pumps: Both gas and electric.

Home Office Equipment: Computers, printers, and other electronics damaged by electrical surges.

Surge Protection: Coverage for electronics and systems damaged by a sudden power surge.

Some policies may also cover items like pool equipment, home theater systems, and even personal medical equipment if damaged in a covered breakdown.

Real-Life Scenarios Where It Helps

1. Power Surge Damage

A sudden power surge knocks out your expensive smart refrigerator. Equipment Breakdown Coverage could help pay for repairs or a replacement.

2. HVAC System Failure

Your air conditioning unit’s compressor fails in July. Without coverage, replacing it could run thousands. With coverage, you may only be responsible for the deductible.

3. Boiler Breakdown

In the middle of winter, your boiler stops working due to a mechanical failure. Coverage can help you get it repaired quickly so you’re not left in the cold.

Why Add It to Your Policy?

Affordable: Often costs a relatively small amount to add to your homeowners insurance.

High Repair Costs: Many household systems cost thousands to repair or replace.

Peace of Mind: Covers many situations not included in standard home insurance.

Equipment Breakdown Coverage

fills a common gap in standard homeowners insurance by protecting your home’s major systems and appliances from sudden mechanical or electrical failures. For a relatively low additional premium, it can save you from hefty repair bills and the inconvenience of being without essential equipment.

Before adding it, review your current policy and talk to your insurance agent about what’s included, what’s excluded, and whether the coverage makes sense for your household. Contact us

for a free estimate for home insurance with equipment breakdown added.

Recent posts

Will Your Auto or Home Insurance Cover Your Mobile Device or Computer? Our phones and laptops aren’t just gadgets anymore, they’re lifelines. From handling business on the go to streaming that must-watch series at night, they’re practically extensions of ourselves. But what happens when the unexpected occurs? A drop, a theft, a spilled cup of coffee, will your auto or home insurance policy swoop in to save the day? Let’s break it down. Home Insurance & Your Tech Good news! Most homeowners and renters insurance policies can cover personal electronics like smartphones, tablets, and computers, at least up to policy limits. Theft or Fire : If your laptop is stolen from your home or damaged in a covered event like a house fire, your policy may reimburse you. Vandalism & Certain Storms : Same deal here. If your tech is damaged by something your policy specifically lists as covered, you’re in luck. But here’s the potential issue: coverage is usually subject to your deductible. If you have a $1,000 deductible and your device is worth $800, you might be out of pocket. 💡 Pro Tip: Ask your agent about scheduled personal property coverage or a rider, these can give your devices extra protection (and sometimes lower deductibles). Auto Insurance & Your Devices This one surprises people. If your phone or laptop is stolen from your car, your auto policy generally doesn’t cover it. Instead, it would fall back to your homeowners or renters insurance. However, your auto insurance can play a role if your car itself is damaged and your devices are harmed in the process. Example: a covered accident shatters your windshield and your laptop sitting in the passenger seat gets smashed. Some policies may extend limited coverage for items damaged inside the vehicle. Still, it’s not the main player here, think of your car insurance as handling the car first and foremost. What’s Not Typically Covered Accidental Damage (a.k.a. Clumsy Drops) : Most standard home or renters insurance won’t pay out if you drop your phone in the pool. Wear & Tear : If your laptop battery dies from age, that’s on you. Manufacturer Defects : That’s what warranties or protection plans are for. How to Make Sure You’re Protected Inventory Your Devices : Keep a running list (and receipts if you have them). Check Your Policy Limits : Electronics often have sub-limits that cap coverage. Consider Add-Ons : Riders or endorsements can provide stronger coverage for today’s high-ticket devices. Device Protection Beyond Your Plan While you’re safeguarding your tech, why not protect how you carry it? If you’re in the market for premium, durable, stylish leather accessories, check out our office favorites and get our exclusive 10% discount - Andar – Handcrafted Wallets & Tech Accessories These items don’t replace insurance, but they make sure your phone or computer travels in style and gets treated like the valuable gear it is. The Sonon Insurance Takeaway Insurance is about more than protecting the big stuff like your car or home, it’s also about safeguarding the tools that keep your everyday life running smoothly. If you rely on your devices (and who doesn’t?), make sure your coverage fits your lifestyle. At Sonon Insurance, we’ll walk you through what’s covered, what’s not, and how to fill in the gaps so your laptop or phone doesn’t leave you stranded in the digital stone age. ✅ Affiliate Disclosure & Legal Stuff We want to be transparent: some of the product links in this post are affiliate links—meaning Sonon Insurance may earn a commission if you click through and make a purchase. This comes at no extra cost to you, and we only promote products we genuinely believe will provide value. We’re not responsible for warranties, returns, or damage once the product is in your hands—any such policies come from the product brand itself.

Gap Insurance: Dealer Add-On vs. Auto Insurance Policy — Which Is the Smarter Choice? Buying a new car is exciting, but it also comes with financial risks. The moment you drive off the lot, your vehicle starts to depreciate in value. If your car is ever totaled or stolen, your standard auto insurance typically pays out the actual cash value, not the balance left on your loan or lease. That’s where Gap Insurance comes in. Short for Guaranteed Asset Protection, it covers the “gap” between what your vehicle is worth and what you still owe your lender. Why You’ll Hear About Gap Insurance at the Dealership When you’re finalizing your purchase, the finance manager often offers Gap Insurance as an add-on. Convenience : You can roll it right into your financing paperwork. Cost : This convenience comes at a price. Dealers typically charge $400– $900 as a one-time fee, and because it’s financed, you’ll also pay interest on it. Commitment : Once it’s bundled into your loan, you’re locked into that cost even if your balance drops faster than expected. For example: if you buy a $30,000 SUV and total it a year later when it’s worth only $24,000, but you still owe $28,000, the dealer’s Gap Insurance would cover the $4,000 difference. Useful—but not always cost-effective. Gap Insurance Through Your Auto Insurance Policy What many car buyers don’t realize is that they can add Gap Insurance directly to their auto insurance policy. Lower Cost : Most carriers charge just $20–$40 per year for the same protection. Flexibility : You can add or remove the coverage as your loan balance changes. Same Protection : It covers the same difference between your loan and your vehicle’s actual cash value. In the SUV example above, adding Gap Insurance through your policy would provide the same $4,000 protection—but at a fraction of the cost. Which Option Is Best? If you like convenience and don’t mind paying more, the dealership option works. If you want long-term savings, adding Gap Insurance to your auto policy is almost always the smarter financial choice. At Sonon Insurance , you can explore whether adding Gap Insurance to your auto policy makes more sense for your wallet. Because protecting your vehicle, and your finances, shouldn’t cost more than it has to.